Understanding how debt cycles function—the intervals between financial collapses—is crucial for anticipating the next economic downturn.

Governments and central banks strive to predict debt crises and navigate them successfully. For investors like us, the goal is to recognize these cycles and capitalize on them.

Historical patterns show that we are approaching another debt crisis. Events leading to major economic downturns, like the Great Depression in 1929, Japan’s bubble burst in 1988, the dot-com crash in 2000, or the Great Recession in 2008, all exhibited early signs of a looming debt crisis.

Ray Dalio’s theories help us understand why we’re on the brink of another debt disaster and how investors can prepare.

Debt Cycles Explained Economies exhibit predictable long-term and short-term debt cycles. Short-term cycles typically span about 12 years, marked by a pattern of boom-and-bust: periods of affluence and overspending followed by austerity and cautious spending.

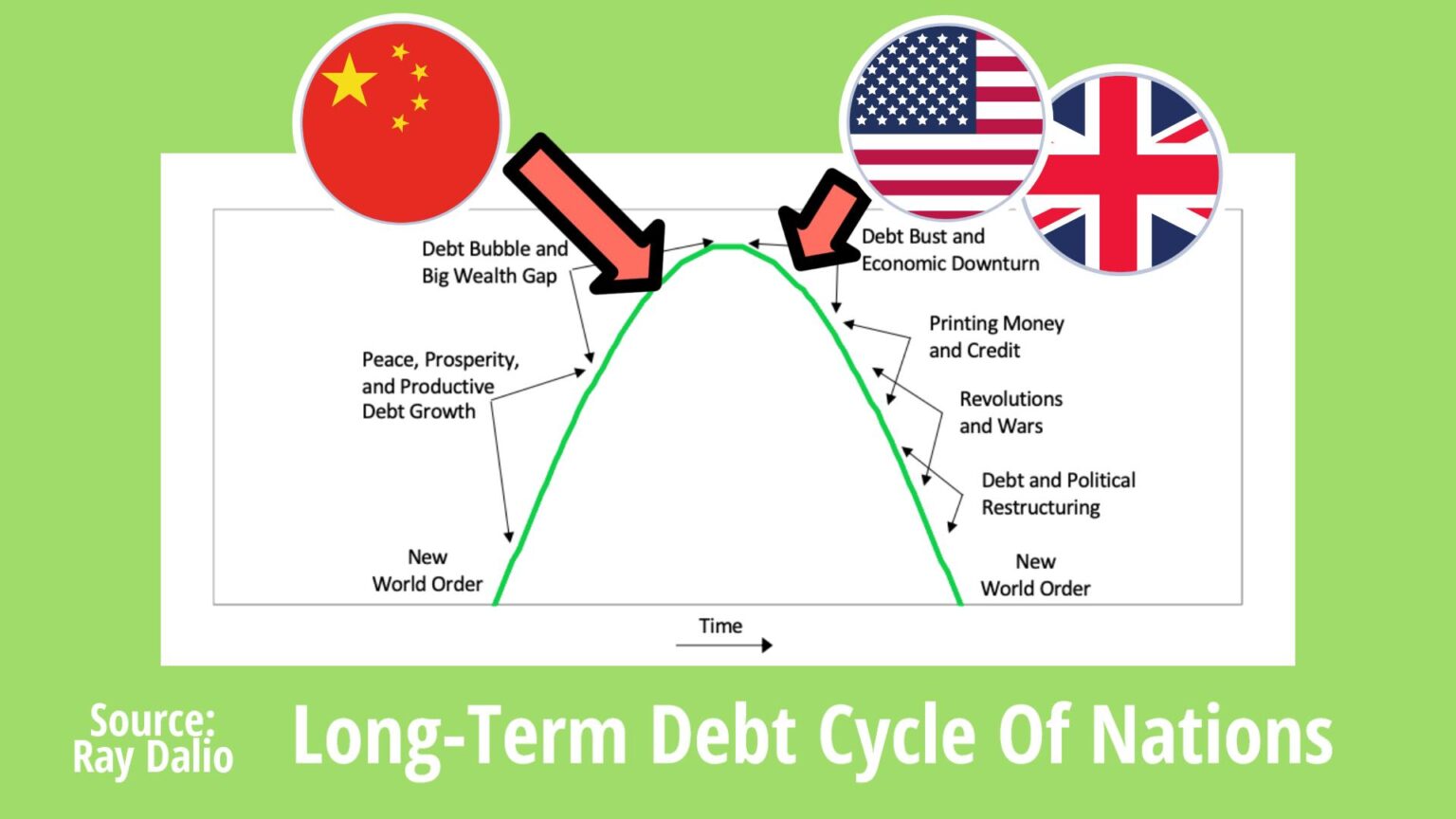

Long-term cycles last much longer, around 75 years, often mirroring a country’s rise to prominence and eventual decline.

Stages of Long-Term Debt Cycle – Inspired by Ray Dalio Countries like China are on the rise, experiencing decreasing wealth inequality and using credit to build infrastructure and fuel growth. In contrast, Ray Dalio views countries like America and the UK as past their prime, with their economies increasingly reliant on monetary expansion to sustain growth.

Deflationary Debt Cycles in the West In Western countries, debt cycles are typically deflationary. In such crises, investment assets lose value, and gold becomes a safe haven.

Conversely, inflationary debt crises, like post-World War I Germany, can lead to hyperinflation. If you are like me, you are experiencing the pain of inflation everwhere!

Credit Dynamics What is often perceived as money is actually credit. You can purchase items using a credit card, but essentially, you’re providing a promise to pay the bank later. When a debt crisis crashes and you’re unable to pay off the card, it becomes evident that this money never truly existed and has vanished from the economy.

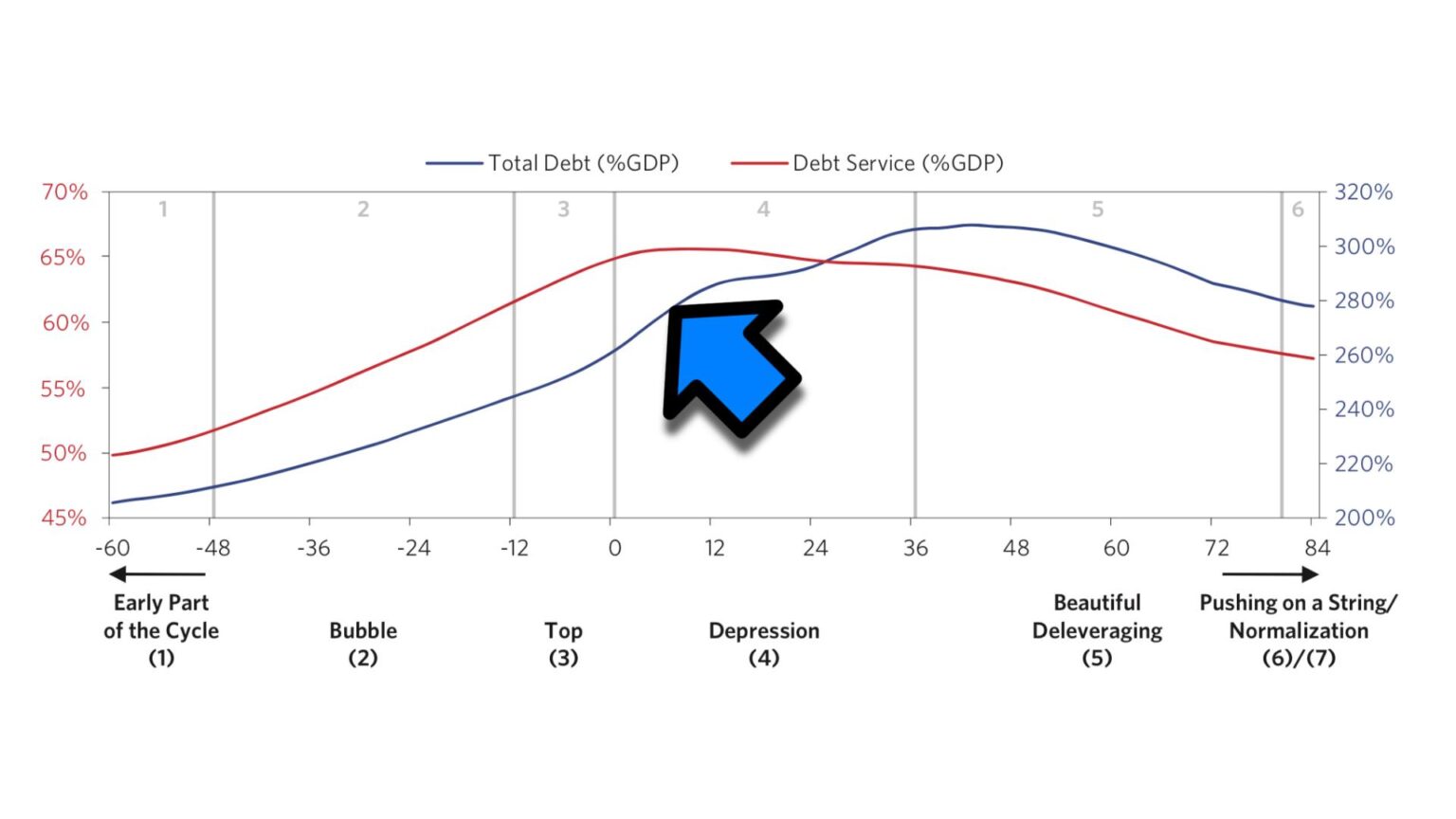

Short-Term Debt Cycles Credit is essential for economic growth during prosperous times. People increasingly use credit because growth opportunities are abundant. Banks are eager to lend as profits are high.

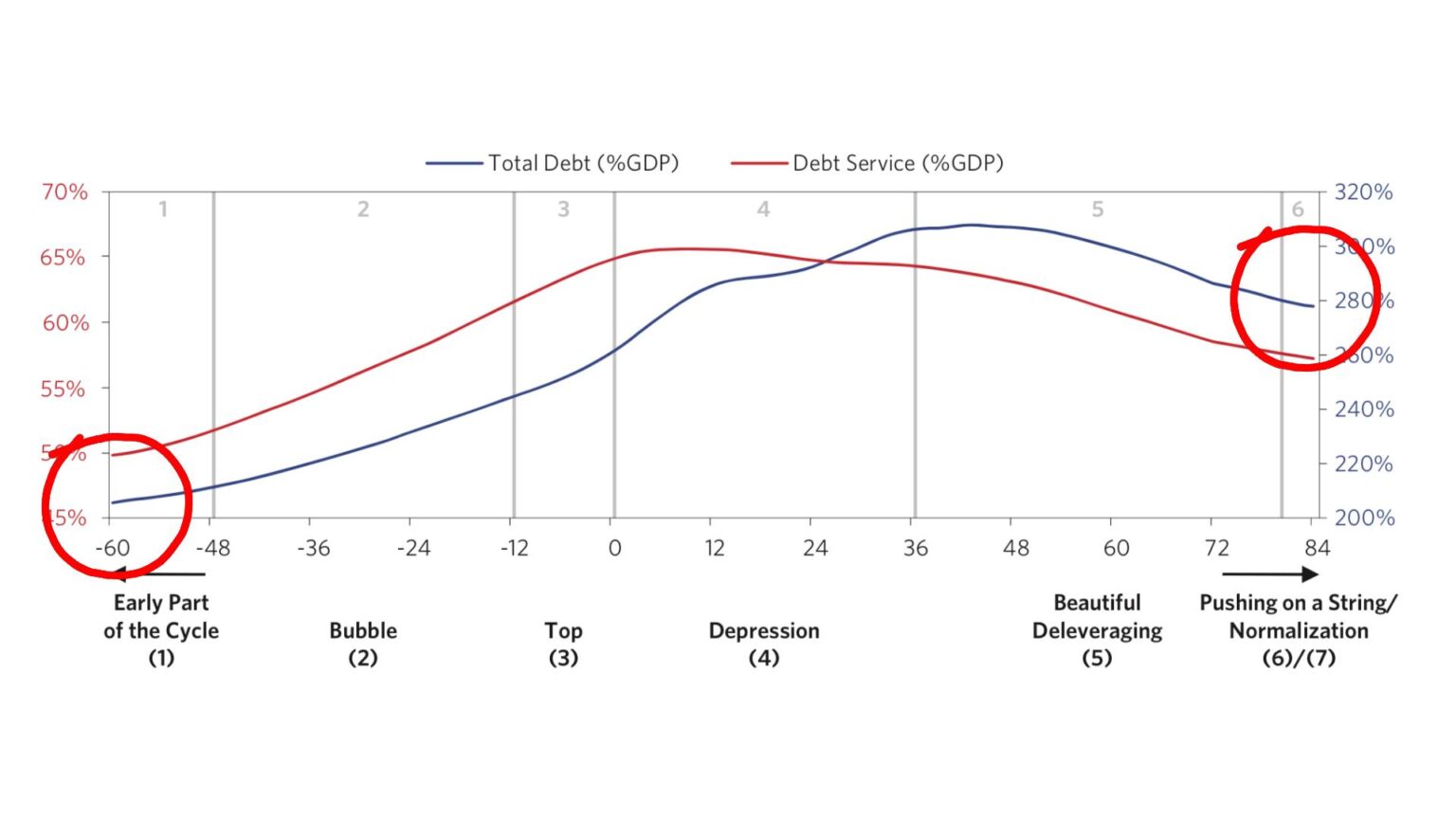

Above is a typical short-term debt cycle as described in Ray Dalio’s “Big Debt Crises.” The cycle spans about 12 years, from recovery through a bubble phase to a decline and debt deleveraging. The key metric is total debt as a percentage of GDP.

2020-2021: A Prelude to Deleveraging This period fits into the depression phase following a prosperous late 2010s, peaking in Debt-to-GDP ratio and exacerbated by massive monetary expansion during the COVID-19 crisis. We’re approaching a phase where debt must be reduced, regardless of the pain, due to its unsustainability.

How to Manage Debt Crises There are five primary strategies to manage a debt crisis:

-

Austerity: Tried with limited success post-2008, austerity is deflationary and can hinder growth.

-

Debt Cancellations: Cancelling debt can be necessary but detrimental to lenders, potentially exacerbating a deflationary spiral.

-

Slash Interest Rates: Lowering rates eases the burden of debt interest payments and discourages hoarding money in savings, thus stimulating investment.

-

The Magic Money Tree: Central banks print more money, effective if debts are in the local currency, but this can lead to future currency issues.

-

Raise Taxes: Necessary to address national debts but harmful during a crisis as it reduces everyone’s spending power.

Long-Term Debt Cycles and the Coming Crisis Each short-term cycle leaves the country more indebted, and after several cycles, this culminates in a significant crash like the Great Depression. The tools used to resolve past crises are becoming less effective.

Interest rates are near zero, and monetary policies are exhausted. The UK, with its debt over £2.6 trillion, has little room to maneuver for the next crisis, potentially leading to a disaster akin to 1929.

Investor Strategies During Debt Crises During growth periods, assets like stocks and property are preferred. In debt crises, these assets decline in productivity, and money shifts to cash and precious metals like gold and silver.

Are Debt Crises Inevitable? Almost. Credit is rarely managed perfectly and often poorly. Short-term growth funded by credit is politically easier than imposing austerity or restrictions before a crash.

Why Now is the Time to Own Physical Precious Metals In the current climate, where signs point towards an impending debt crisis collapse and traditional asset classes may falter, owning physical precious metals can be a sound defensive strategy.

Here’s why:

-

Historical Safety Net: Gold and silver have historically performed well during economic downturns, serving as a hedge against both inflation and deflation.

-

Limited Room for Monetary Policy Maneuver: Regardless of interest rates, government debt at all time highs, central banks have fewer options to stimulate the economy without causing further issues, making precious metals an attractive store of value.

-

Diversification: Adding precious metals to your investment portfolio can reduce risk and increase resilience against market volatility.

-

Physical Security: Unlike digital assets or stocks, physical precious metals can’t be erased or hacked, offering tangible security in uncertain times.

-

Intrinsic Value: Precious metals carry intrinsic value due to their utility and rarity, maintaining purchasing power over time, unlike fiat currencies, which can be devalued by excessive printing.

As we navigate our current historic debt crisis, the strategic acquisition of physical precious metals can provide both security and potential for capital preservation in your investment strategy.