In recent weeks, the world has turned its attention to China’s ailing economy as the country unveiled a significant economic stimulus package to reverse a steep downturn. However, despite these measures, deeper concerns loom over the effectiveness of the stimulus in preventing what appears to be an imminent recession.

Let’s take a closer look at how China’s current crisis unfolded and why the recent wave of stimulus might not be enough to save the world’s second-largest economy.

China’s Economic Troubles Began with a Real Estate Collapse

At the heart of China’s economic woes is its real estate market, which has faced a sharp and dramatic collapse. The most notable event was the bankruptcy of Evergrande, one of China’s largest real estate developers. Evergrande’s default sent shockwaves across the global financial markets, making investors realize just how deep the problems ran in China’s property sector.

The collapse in real estate has been profound. China’s real estate index is now down over 80% from its recent highs, falling to levels below the 2008 financial crisis. The real estate sector has long been a pillar of the Chinese economy, accounting for a significant portion of GDP, local government revenue, and household wealth. A downturn of this magnitude spells serious trouble for the broader economy.

Deflation: A Sign of Deepening Economic Problems

While most of the world is battling rampant inflation, China faces an entirely different challenge: deflation. Over the last five quarters, prices in China have declined, as seen in the country’s GDP deflator. This is a major indicator of weakening demand, as businesses and consumers pull back on spending.

Deflation is often a sign of an economic contraction. In China’s case, it highlights the depth of the economic slowdown. When prices fall over an extended period, profits decrease, wages stagnate, and unemployment rises. This creates a vicious cycle where people hold off on making purchases, anticipating that prices will fall further, thereby worsening the downturn.

China’s Response: A Massive Stimulus Package

In response to these mounting issues, China introduced several key stimulus measures:

-

Cutting reserve requirements by 0.5% to encourage more bank lending.

-

A 0.2% cut in the 7-day reverse repo rate to increase liquidity.

-

Lowering mortgage rates to stimulate demand in the real estate market.

-

Injecting $142 billion into banks to provide more lending power.

-

Implementing ‘forceful’ interest rate cuts.

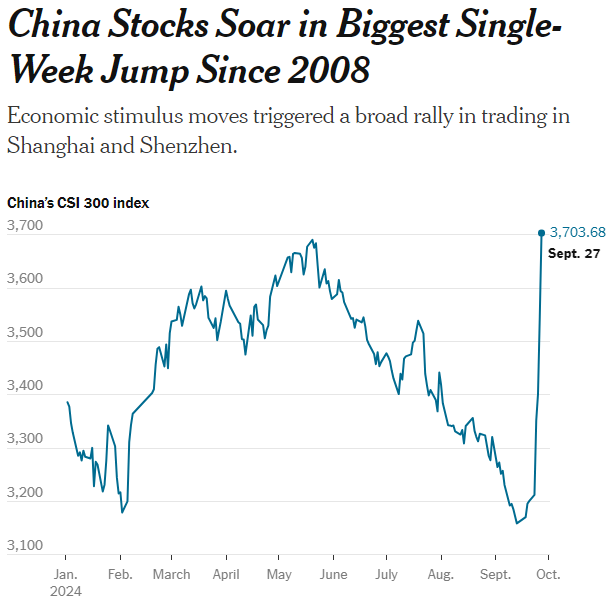

The reaction from the stock market was swift. China’s CSI 300 Index soared by its biggest single-week gain since 2008, as retail investors piled into stocks, hopeful that this stimulus could revive the economy. Brokerages even stayed open around the clock to accommodate a surge of new traders eager to capitalize on the market rally.

But while this market rally may seem promising, the question remains: Is this just temporary, or will these stimulus measures lead to sustained recovery?

Stimulus Alone May Not Be Enough

As many countries learned during the 2020 lockdowns, stimulus alone may not be enough to revive an economy if underlying structural issues persist. China’s real estate market continues to suffer, and confidence in the economy remains low. Both consumers and businesses are holding back, waiting to see whether conditions will improve.

One of the most worrying signs is that nominal GDP is expected to contract in China. This is a strong indicator that the economy could slip into a recession, something that could be devastating not only for China but for the global economy as well.

Furthermore, M1 money supply—a measure of the amount of money circulating in the economy—has been dropping. The decline in M1 is driven by weak demand for credit and central bank efforts to tighten liquidity. Without robust credit growth, it’s unlikely that businesses and consumers will have the confidence to spend, invest, and borrow—key factors needed to kickstart an economic recovery.

The Long Road Ahead for China

The challenges China faces are significant, and it’s clear that the stimulus measures introduced in recent weeks may not be enough to stave off a recession. With both nominal GDP and M1 money supply in decline, the country is likely heading for a prolonged downturn unless confidence is restored and more substantial structural reforms are made.

What’s Next?

To prevent a recession, China will need to go beyond just stimulus. A serious restructuring of its real estate sector and banking system is required. Confidence must be restored, not just through liquidity injections but through meaningful reforms that address the root causes of deflation and economic contraction.

Without these changes, China may be heading toward a prolonged recession that could last well into 2026.

The world is watching closely as China navigates one of the most challenging economic periods in its modern history. Only time will tell whether the measures taken now will be enough to pull the country back from the brink.

Conclusion

China’s current crisis is a stark reminder that economies cannot rely solely on short-term stimulus measures to navigate structural problems. The depth of the country’s real estate collapse, combined with deflation and weak credit demand, suggests that the road to recovery will be long and uncertain. For now, all eyes remain on whether China can implement the necessary reforms to stabilize its economy and avoid a prolonged recession.