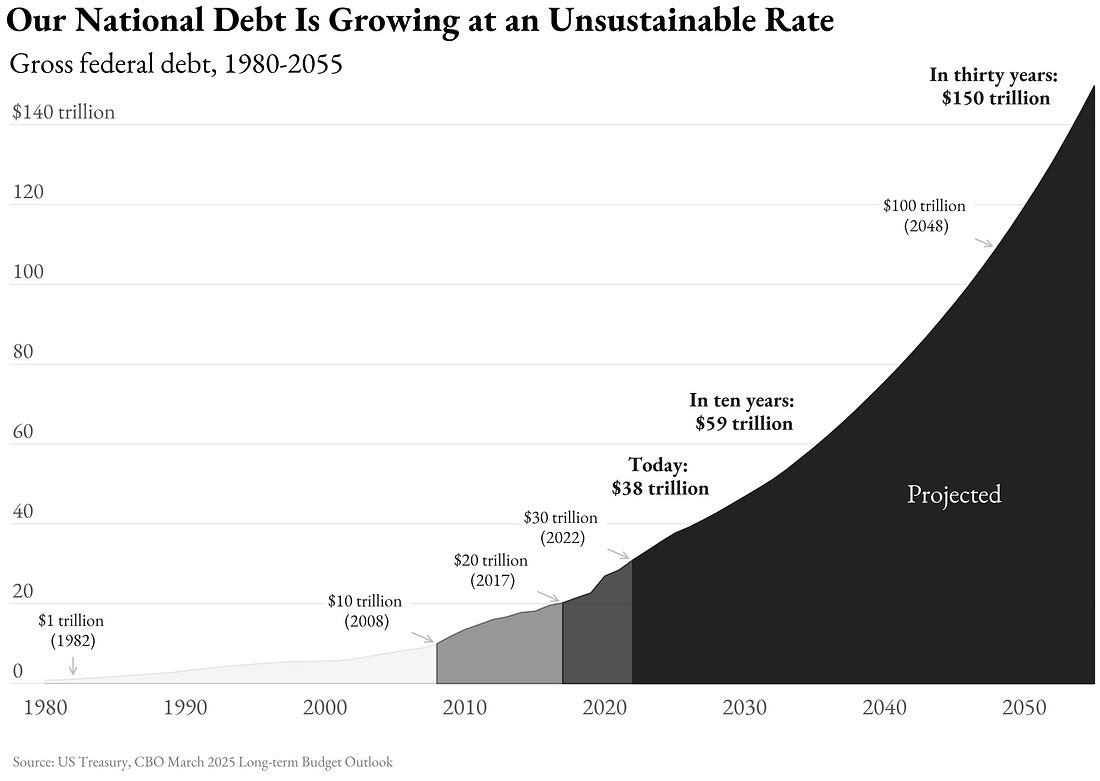

The chart above tells a simple but profound story: U.S. government debt is no longer growing linearly—it’s compounding. According to long-term projections, federal debt rises from roughly $38 trillion today to $59 trillion within ten years, crosses $100 trillion around 2048, and approaches $150 trillion thereafter.

This matters enormously for precious metals investors because debt does not exist in isolation. It directly shapes monetary policy, interest rates, currency purchasing power, and investor behavior. When viewed through that lens, this debt trajectory is structurally bullish for gold, silver, and platinum.

Below is the framework we use to understand why.

⸻

1. Unsustainable Debt Forces Monetary Debasement

At these levels, debt cannot be “paid down” in any traditional sense. The only politically viable paths forward are:

• Currency debasement (printing money)

• Financial repression (rates below inflation)

• Inflationary erosion of real debt value

Historically, governments choose the least visible option: devalue the currency rather than default outright.

Precious metals thrive in this environment because:

• They cannot be printed

• They reprice higher as currency purchasing power falls

• They exist outside the debt-based financial system

Gold, in particular, has served for thousands of years as a barometer of confidence in fiat money.

⸻

2. Debt Growth Caps Interest Rates (Even When Inflation Is High)

With debt this large, high interest rates become mathematically impossible.

Every percentage-point increase in rates dramatically raises:

• Government interest expense

• Budget deficits

• The need for even more borrowing

This creates a trap:

• Rates must stay artificially low

• Inflation remains structurally elevated

• Real yields stay negative

Negative real rates are historically one of the strongest bullish drivers for gold and silver. When savers lose purchasing power by holding cash or bonds, capital flows toward hard assets.

⸻

3. Debt Expansion Weakens the Dollar Long-Term

While the U.S. dollar may remain strong relative to other currencies at times, its purchasing power continues to erode.

Debt-driven systems require:

• More dollars to service old dollars

• Larger deficits to sustain growth

• Ever-expanding money supply

This is why:

• Gold has risen dramatically since the U.S. left the gold standard

• Central banks around the world are accumulating gold at record levels

• Nations are quietly reducing reliance on U.S. Treasuries

Gold and silver act as currency alternatives when trust in fiat systems declines.

⸻

4. Precious Metals Are a Direct Hedge Against Policy Risk

This chart represents not just numbers—but policy risk.

As debt climbs, policymakers face fewer good options and more extreme ones:

• Yield curve control

• Capital controls

• Wealth taxes

• Changes to retirement rules

• Forced participation in government debt markets

Physical precious metals—especially when held properly—sit outside these policy levers.

They represent:

• No counterparty risk

• No default risk

• No dependency on financial institutions

• No liability of another party

That’s why metals tend to perform best when confidence in institutions weakens.

⸻

5. Silver & Platinum Add Leverage to the Thesis

While gold is the monetary anchor, silver and platinum provide asymmetric upside:

• Silver historically outperforms gold during strong inflationary and monetary cycles due to its smaller market size and dual monetary/industrial role.

• Platinum adds diversification and optional upside tied to industrial demand and supply constraints, while still behaving as a hard asset.

In debt-driven inflationary regimes, diversification within precious metals matters.

⸻

6. This Is Not a Short-Term Trade—It’s a Structural Trend

The key takeaway from the chart is trajectory, not timing.

Debt on this scale:

• Cannot be reversed politically

• Cannot be refinanced indefinitely at market rates

• Cannot coexist with sound money

That’s why precious metals are not a “trade” here—they are a strategic allocation designed to:

• Preserve purchasing power

• Reduce reliance on financial promises

• Provide optionality in uncertain times

⸻

Bottom Line

The projected U.S. debt path reinforces a core truth:

When governments over borrow, currencies eventually pay the price—and hard assets reassert their role as stores of value.

Gold, silver, and platinum are not betting against America—they are hedging against math and incentives.

This debt curve makes precious metals not just relevant, but necessary as part of a prudent long-term strategy.

If you’d like, I can follow this post with:

• A historical comparison (1970s, post-WWII, post-2008)

• A breakdown of which metals benefit most at each phase

• A portfolio allocation framework for navigating the next decade